Faes Farma's reinvention is not ordinary

Who would have believed that amongst the star-studded European pharma names, the tiny (in market cap terms, relative to Big Pharmas) Faes Farma (ADD; Spain) would be a massive outperformer over a two-year timeframe. For the uninitiated, Faes has been contending with the loss of European patents for its key antihistamine (used against allergies, cold, etc.) molecule Bilastine (c.21% of sales) in 2021-22 and slowing demand from its main market Spain (c.28% of sales; +0.1% in 2025).

Outstanding re-rating …

… backed by bold (internal and external) bets

Over 2021-24, a slowdown in Spain and struggles of the animal nutrition segment (c.13% of sales), were more than compensated by expanding business in ‘International’ markets (i.e., outside Spain and Portugal; c.33%), and healthy growth in Licensing business (c.18%). Remember, amid the maturing market for firm’s products in Europe, Faes’ pivot towards LatAm (averaging c.15% growth over 2021-25) has proven to be a game changer.

Nonetheless, the markets’ enthusiasm around Faes’ prospects, especially from 2025 onwards, was influenced by a cocktail of the following factors.

While Donald Trump’s tariff policies created uncertainties for most European pharmas in early 2025, Faes Farma was a relative beneficiary because of its lack of direct exposure to the US markets. The other area of investors’ concern, i.e., mid-to-long term growth, was addressed by the firm being aggressive in chasing external opportunities. In March and June 2025, the firm announced biggish acquisitions of Portuguese and Italian ophthalmology firms, Edol and SIFI (worth c.18% of Faes’ current market cap), respectively. These deals not only compensated for the firm’s weak pipeline, but also diversified its exposure, away from mainly antihistamines, vitamin D supplement (Calcifediol) and inflammatory bowel disease treatment (Mesalazine). From 2026 onwards, ophthalmology could contribute c.20% of the group sales. In addition, with an ageing global population, growing incidence of diabetes, a rise in seasonal allergies, and increasing use of screens, ophthalmology is anticipated to grow by mid-single digits in the medium term. The pivot towards ophthalmology is a smart move, as these medicines often treat chronic conditions with repeat prescriptions.

Even before the SIFI acquisition was announced, the management, in April 2025, revealed their mid-term ambitions of doubling the sales (vs. 2024 levels) by 2030, via organic as well as inorganic means, i.e., 8-9% organic CAGR and 11-12% including acquisitions. Also, EBITDA is envisioned to expand at 7-8% CAGR over 2024-30 (10-11% including M&A). Interestingly, these targets exceeded the street’s expectations from Faes.

Lastly, the Animal nutrition business, which struggled over 2021-24 (averaging c.5% sales decline), wildly sprung back to life in 2025 (+52% sales growth), thanks to the new ISF (specialised feed for pigs) plant (started contributing from late-2024 onwards), which resolved the production capacity bottleneck. This solid performance was despite the restrained female pig population in Spain – impacted by outbreaks of PRRS (Porcine Reproductive and Respiratory Syndrome) – and pricing pressure on Spanish pork because of Chinese tariffs.

Growth prospects better than many sectoral peers

Ironically, despite being not amongst the top innovative pharmas, Faes’ mid-term growth prospects (>11% bottom-line CAGR expected over 2025-27) are ahead of quite a few in the industry. While the firm showed €5.8m (1.3% of sales) of R&D expenses on its 2024 income statement (2025 figures are yet to be released), it capitalises most of its research and development work. In fact, the total R&D investment in 2024 amounted to €25m or 5.5% of sales. Faes aims to improve this ratio to 10% by 2030, thereby gradually strengthening its innovation quotient.

In the mid-term, growth should be driven by 1/ enlarged manufacturing capacity (via Derio plant for pharma medicines and Huesca site for animal nutrition business; both in Spain); 2/ the firm’s incremental innovation and lifecycle management of existing key molecules, i.e., Bilastine, Calcifediol (c.10% of sales) and Mesalazine (c.3%); 3/ expansion into markets outside Europe; and 4/ external innovation.

The nearly €200m investment (for context, c.13% of current market cap; funded by internal resources) in Derio plant over 2021-24 doubles the firm’s manufacturing capacity, increases control over product quality, removes growth bottlenecks and supports margins in the coming years.

Interestingly, despite Bilastine’s patent expiry in European markets a few years ago, the firm has managed well its life cycle via licensing in newer geographies (available in >100 countries) and newer formulations. In 2023, Faes launched eye drops and orodispersible tablets of Bilastine, and now the drug’s paediatric formulation for children under 6 in Europe should enter a segment traditionally dominated by cetirizine and loratadine. Coming to Calcifediol, there is a massive need for Vitamin D supplements in Faes' countries of interest. In Spain, >50% of the population is Vitamin D deficient, and the figure could be even higher in LatAm. Remember that a Vitamin D deficiency can cause osteoporosis (wherein bones become fragile), lead to cardiovascular problems and even other autoimmune diseases. In fact, the management expects incremental innovation in three main molecules to contribute c.35% of these molecules’ 2030 sales.

Considering Faes’ constraints around commercial reach, it has been leveraging its key molecules’ (mainly Bilastine) potential via the licensing business. This approach fetches high-margin and recurring sales for the firm, without much capital outlay. The licensing business should act as a stability provider in the mid-term.

Finally, despite capital outlays in the recent years, the balance sheet remains healthy (2026e net debt-to-EBITDA of 1.8x) and Faes’ cash generating ability (FCF yield averaging >5% over 2026-27) should make way for further acquisitions in the next couple of years. In addition, the current price offers a decent dividend yield (c.3%).

Hold your horses for more upside

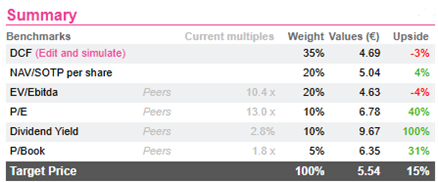

Besides the above-mentioned aspects, the firm also improved its governance when it separated the roles of Chairman and CEO in 2024. However, considering the c.75% share price run in the last two years, most of the growth story seems priced in currently. Faes’ 2026e P/E of c.14x is even better than that of Sanofi (BUY; France) and GSK (Reduce; UK). While we foresee c.15% upside in Faes, it’s worth waiting for a broader-market-driven correction for a bigger upside in this Spanish stock.

Subscribe to our blog

AlphaValue's Fundamental Strength Indicator reveals 24 "unsinkable" business mo...

A $330 share price, 40x earnings expected five years from now, and growth funded by SoftBank: wh...