Fireworks of Metal

This is a train that AlphaValue boarded timely: metals at large have been on fire, courtesy of … God only knows actually. Say hyperscalers and their capex on steroids, CBAM for Europe, gold arbitrage, US this time leading the race piling up copper.

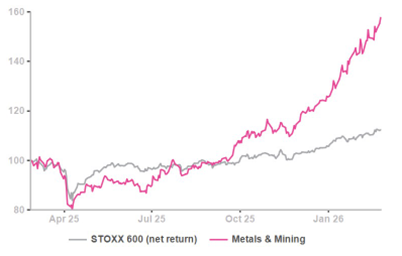

Ytd Metals & Mining left every single sector in the dust, but for Semiconductors.

Obviously, there is nothing in common between Arcelor and South32 or Aurubis. The ytd excitement is very widely based, suggesting that it is not driven by stock specific profitability changes. The excitement is thus unlikely to be robust. Rates expectations do not seem to be a driver. The most likely acceptable explanation is capital spending, as accelerated by AI compute needs, and metals/commos being a port of call if markets were to enter a moment of doubt.

We have kept a towering view of the sector for the next few lines, as we wonder when it is right to bow out.

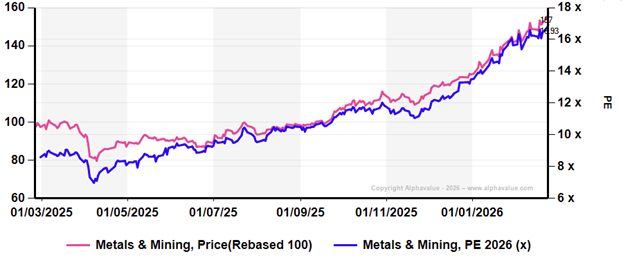

A good starting point is that for now the rise is a case of multiple expansion, as 2026 PEs have nearly doubled (see chart below) to 17x.

Metals & Mining index (pink) and related PE (blue)

Even more perplexing is the lack of oomph in earnings revisions. Here is a telling table which suggests that 2026 earnings are not exactly being upgraded, at least for now. Worse, the expected 2026 earnings a year ago, were 25% above the current. Over the long run, the sector chugs along with earnings between €35bn and €40bn. Not enough of a positive dynamic here to a take a plunge.

No earnings upgrade so far

So time to take profits? Yes. Antofagasta, Outokumpu, Boliden, Aurubis, Tenaris, Anglo American all look dear now.

Metals & Mining valuation table

Ytd Metals & Mining left every single sector in the dust, but for Semiconductors.

Obviously, there is nothing in common between Arcelor and South32 or Aurubis. The ytd excitement is very widely based, suggesting that it is not driven by stock specific profitability changes. The excitement is thus unlikely to be robust. Rates expectations do not seem to be a driver. The most likely acceptable explanation is capital spending, as accelerated by AI compute needs, and metals/commos being a port of call if markets were to enter a moment of doubt.

We have kept a towering view of the sector for the next few lines, as we wonder when it is right to bow out.

A good starting point is that for now the rise is a case of multiple expansion, as 2026 PEs have nearly doubled (see chart below) to 17x.

Metals & Mining index (pink) and related PE (blue)

Even more perplexing is the lack of oomph in earnings revisions. Here is a telling table which suggests that 2026 earnings are not exactly being upgraded, at least for now. Worse, the expected 2026 earnings a year ago, were 25% above the current. Over the long run, the sector chugs along with earnings between €35bn and €40bn. Not enough of a positive dynamic here to a take a plunge.

No earnings upgrade so far

So time to take profits? Yes. Antofagasta, Outokumpu, Boliden, Aurubis, Tenaris, Anglo American all look dear now.

Metals & Mining valuation table

Subscribe to our blog

AlphaValue's Fundamental Strength Indicator reveals 24 "unsinkable" business mo...

A $330 share price, 40x earnings expected five years from now, and growth funded by SoftBank: wh...