Jeronimo Martins

Note: This is a daily stock update and the information stands true as of 19/03/26, 09:00 CET.

Company Update:

Following its Q4 trading update released in January 2026, Jeronimo Martins has now reported full-year results that came in ahead of market expectations.

Following its Q4 trading update released in January 2026, Jeronimo Martins has now reported full-year results that came in ahead of market expectations.

In Q4, the group’s EBIT rose 12% year-on-year to €374m, beating consensus by 10.3%. Adjusted EPS (excluding other profit/loss) was €0.35 per share, also 9.4% above street estimates.

For the full year, adjusted EPS and DPS were €1.21 and €0.65 per share, respectively – both exceeding market expectations.

However, management did not provide quantified guidance for 2026 and cautioned about rising geopolitical tensions, noting that the impact on energy prices and food inflation remains uncertain. The CEO also highlighted that Biedronka, the group’s key profit driver, has entered the year in a deflationary environment.

These comments may weigh on investor sentiment. While we are likely to make modest adjustments to our financial forecasts and target price, we believe that despite near-term headwinds, Jeronimo Martins remains an attractive business with a compelling valuation.

Expert Opinion:

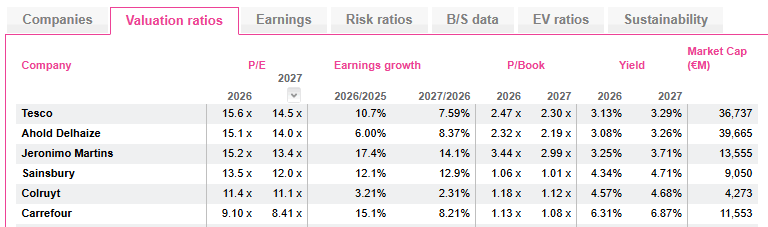

Jeronimo Martins remains a compelling story in the European food retail with organic growth structurally above peers. Yet it only trades at a slight premium to peers (and below Tesco's valuation ratios). We still see Food retail as a defensive sector in the current situation as food spendings are constrained and cannot be massively cut. Despite its recent share price performance, we still like Carrefour which trades at a massive discount to peers, which isn't fully justified in our opinion.

For daily updates, subscribe to our newsletter and for detailed information, reach out to us at sales@alphavalue.eu

Jeronimo Martins remains a compelling story in the European food retail with organic growth structurally above peers. Yet it only trades at a slight premium to peers (and below Tesco's valuation ratios). We still see Food retail as a defensive sector in the current situation as food spendings are constrained and cannot be massively cut. Despite its recent share price performance, we still like Carrefour which trades at a massive discount to peers, which isn't fully justified in our opinion.

For daily updates, subscribe to our newsletter and for detailed information, reach out to us at sales@alphavalue.eu

Subscribe to our blog

Alphavalue Morning Market Tip

Weak Q2 results and FY guidance (marginally) cut but a fat 9.4 % div yield.