Defence suddenly competitive

Only two years ago European defence incumbents were expected to sail smoothly into a powerful upcycle of military spending. Then Ukraine surfaced as a competent exporter of the latest in missiles and drones’ innovation. Following this, European start-ups with a biggish AI content entered bids where fast-moving technology mattered most. A rather ordinary ordering process would now face bids from fast-changing alliances, disturbing that very process.

In short the European defence industry is becoming highly competitive. This is amplified by an urge to ramp up faster. JVs or manufacturing partnerships with the car industry are pushing the defence industry increasingly down that route. US defence incumbents are following the same pattern.

Competition is not only increasing within Europe. A growing share of future defence spending may be captured through partnerships involving non-European players, from Turkish drone manufacturers to Gulf-backed defence groups, meaning that higher European defence budgets do not automatically translate into higher profit pools for European incumbents.

The above observation may not be applicable to a submarine or fighter order, which are essentially driven by political considerations, but the direction of travel is clear: this is no longer a cozy industry. This is a departure from 2022-2023 when we looked at defence as pure ramp up problems with fat margins in an oligopoly/monopoly market.

At the same time, Europe continues to struggle to translate political ambitions into industrial integration. Programmes such as FCAS illustrate how national interests, workshare negotiations and sovereignty concerns can prevent the emergence of truly pan-European champions.

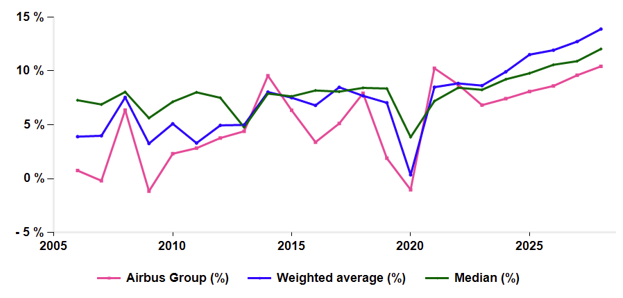

Looking at Ebit margins from 2026 helps gauge the size of the issue. The following chart is in effect the by-product of ‘old ways’ expectations. The blue line shows the sector average margin which up to 2023, had never reached 9%. It is 11.5% in 2025 and counting. The median in green tells a less aggressive margin development. Airbus in pink is here to show that the surge is not theirs.

Aerospace & Defence Ebit margins: 2006-2028

Aerospace & Defence Ebit margins: 2006-2028

The extent of the new competition impact on Ebit margins is obviously hard to gauge. There will be volume gains and a better coverage of fixed costs. R&D costs may well be still largely paid for by governments. But it is clear that the industry is changing its profile to civil like volumes and civil like margins. As a reminder, the Autos industry is hard pressed to post Ebit margins above 6% (leaving aside post Covid scarcity driving them to 9%), and is now looking at less than 5%.

Put differently, the risk may not be lower volumes or weaker demand, but a gradual fragmentation of the industry's profit pool as software, drones, AI-enabled systems and new industrial partnerships attract a broader set of competitors than traditional defence programmes ever did.

Head scratching times indeed.

Subscribe to our blog

AlphaValue's Fundamental Strength Indicator reveals 24 "unsinkable" business mo...

A $330 share price, 40x earnings expected five years from now, and growth funded by SoftBank: wh...