Light steel

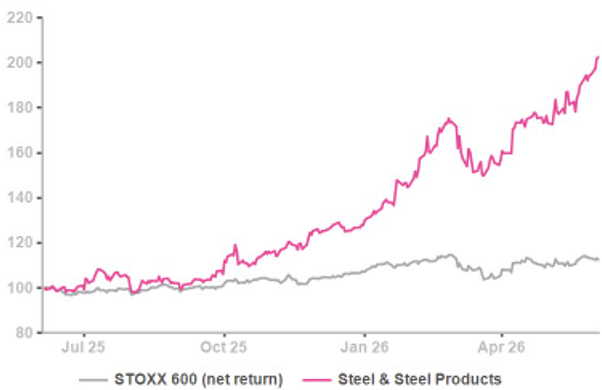

Semiconductors performance chart? No simply European Steel stocks over 1 year

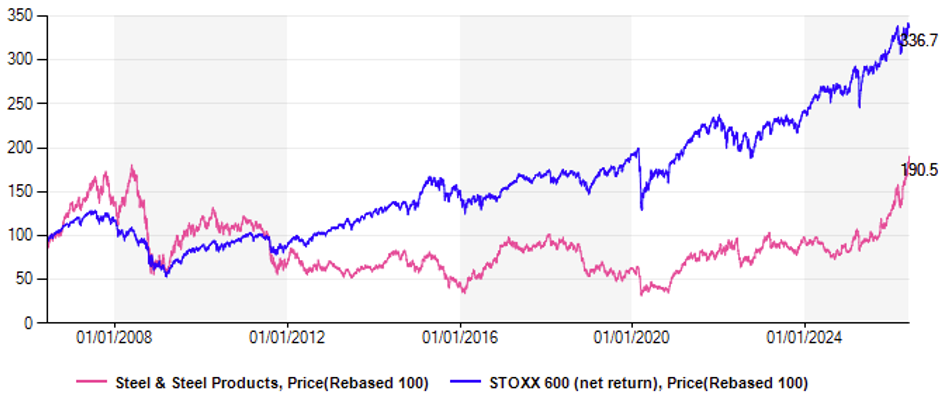

The picture is less impressive over 10 years. We use the equal-weighted performance to cool down the weight of ArcelorMittal.

The picture is less impressive over 10 years. We use the equal-weighted performance to cool down the weight of ArcelorMittal.

As made clear in the ArcelorMittal teaser dated 05-06, the sector surge is not owed to fresh demand. It is owed to European steel users asked to pay more for the stuff as Brussels implemented carbon border taxes on Chinese imports from 01-01-2026.

The positives of closing the door to (polluting & Chinese) competition have been well discounted with the upside potential for the sector being a -2% on a median basis (of note thyssenkrupp is no longer booked as Steel, but as a HoldCo).

The following chart (equal weighted) shows that on an EV/Ebitda basis the sector is not running at unacceptable levels. But there would be no real upside potential either.

Steel sector EV/Ebitda -2006-2028

It is hard to entertain a scenario whereby earnings would go through the roof on increased volumes and prices. Prices are OK in Europe, elsewhere they suffer from China’s massive overcapacity. Betting on earnings upgrades is best left to European semiconductors where eps upgrades are AI driven. Worse the border carbon tax is structurally a fragile frame: good to have but hard to manage and likely to be circumvented.

Our valuations suggest that it is time to pack up. The +40% eps growth for both 2026 and 2027 is volatile by nature in this industry.

Steel valuation essentials

Steel valuation essentials

|

|

Subscribe to our blog

Sanofi looks cheap — but years of R&D setbacks, revolving-door CEOs, and heavy reliance on ...

Markets are cooling on a year of AI-driven speculation as debt funding tightens. AlphaValue expects ...