LVMH handed the baton to ASML. Buy LVMH.

Water utilities are not anybody’s priority and particularly not so when it comes to the handful of UK ones marred by the Thames Water disaster. The cash extraction driven by Thames Water’s private shareholders were of epic proportions, outfoxed the UK regulator and brought about a lot of negative sentiment on the whole UK water industry. In this dramatic context, United Utilities managed to protect its shareholders (if not its customers), and have actually delivered a very respectable performance over the last 10 years.

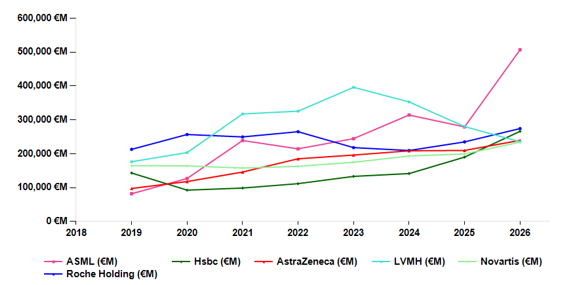

Of course ASML at €500bn sits in another market cap league when compared to LVMH(€235bn). It is worth noting that LVMH is also about to hand over its current position as the European 5th largest market cap to Novartis (€234bn). LVMH led the average market cap league from 2021 to 2023.

Market caps 2019-2026. ASML vs. LVMH and all others. ASML changed gears.

LVMH’s past valuation certainly reflected the absurdity of post-covid yolo-type behaviours. It assumed that everyone and his dog would fall into the trap of luxury necessities.

ASML is in another league, not only in the order of magnitude by its market cap, still a minnow by Nasdaq standards, but about double that of its runner-up (Roche). The above chart also shows that it took 4 years for LVMH to become THE European must-have company with a 28x actual average PE in 2023. Contrast that with ASML, whose rise to the firmament took 6 months and with a prospective PE at 43x, already above its 2024 peak (41x actual).

Only 3 years ago we were wondering about ASML being squeezed in the US/China tussle for technology control. That was Biden’s era. ASML is currently making a fortune while Trump effectively prevented the European company from selling in China. The difference is the US preference that the Trump administration has engineered at great cost to the rest of the nation, but that lines the pockets of the participants in the AI value chain. That includes ASML.

AlphaValue believes in AI, but not in AI’s lack of accountability, whether in terms of capital spending or in terms of egos of founders, detached from reality and turning societies upside down. That will inevitably backfire.

OpenAI, a business with essentially no sales, is bound to be worth $850bn on IPO day. This is hype pricing. With such extreme valuations becoming a new normal, ASLM, at the root of frontier processor manufacturing with sales of c. €39bn, might well deserve its €510bn ($600bn) market cap. But the very speed of the awakening of investors to the virtues of ASML is too weird to hold.

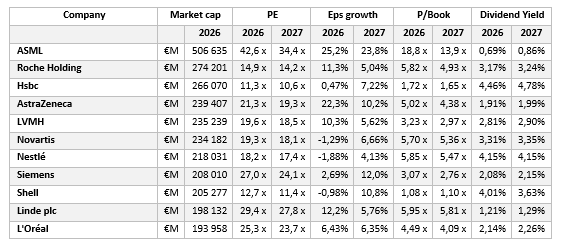

We would suggest to start booking profits on ASML by 5% tranches, and start investing in the 10 companies that follow by market cap. Here is the list:

Subscribe to our blog

Sanofi looks cheap — but years of R&D setbacks, revolving-door CEOs, and heavy reliance on ...

Markets are cooling on a year of AI-driven speculation as debt funding tightens. AlphaValue expects ...