Sandoz's escape velocity deserves ovation

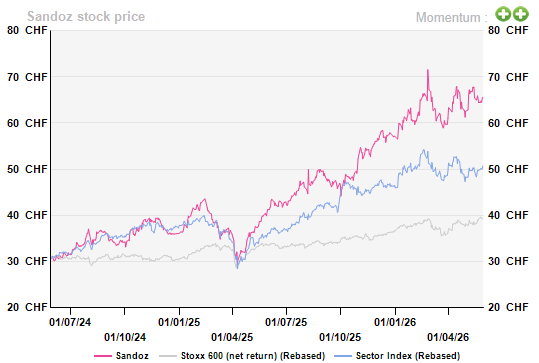

At a time when a lot of Big Pharmas are losing sleep because of looming patent expirations over the next five years, the likes of Sandoz (REDUCE; Switzerland), i.e., generic/biosimilar players, are smiling/excited about the same issue. Besides being able to produce copies of the off-patent originator drugs, there is one more nuance that favours these players – the burgeoning market for biosimilars, medicines that are similar (in efficacy and tolerability) to the originator biologic drugs, made from living cells/organisms. A near tripling of Sandoz’s share price since its public-listing in October 2023 as a Novartis spin-off, owes to its expertise and commanding position in biosimilars.

While generics account for 69% of Sandoz’s topline, the investment story remains centred around biosimilars (31%).

Handsome value creation

Massive scope for further market growth

Massive scope for further market growth

Interestingly, from just about a fifth of the global pharma market in 2010, the value share of the biologic medicines has expanded to mid-40s now. The direction of travel should remain the same in the foreseeable future, since biologic medicines often provide better efficacy, precision and lesser side-effects than chemically-synthesised small molecule drugs. Now when these drugs lose exclusivity, the biosimilar players make merry. With biologic drugs worth c.$320bn sales set to lose exclusivity over the next decade, we do not see an exaggeration in Sandoz calling it a ‘golden’ decade. In fact, we envisage the roughly $35-40bn biosimilar market to expand at a mid-teens percentage in the mid-term, as it should play a major role in keeping a lid on governments’ healthcare costs.

A moat that is difficult to replicate

The Swiss giant’s competitive advantage lies in its development, manufacturing and commercialisation capabilities for biosimilars (and even generics).

Out of hundreds of generic/biosimilar firms, only a fraction are competent enough to truly develop biosimilars. This is because biosimilars are scientifically more complex than generics. For instance, aspirin has roughly 20 atoms, whereas monoclonal antibodies that treat cancer and autoimmune diseases have >20,000 atoms. Moreover, even the biosimilar manufacturing process is part of the moat, as the know-how to keep the molecules stable, uncontaminated and scalable must be learned over the years, and is difficult to transfer across organisations.

Sandoz, having been part of the Novartis (ADD; Switzerland) for decades, is a pioneer in biosimilars and is scientifically strong, not just in developing them, but also in their manufacturing (largely internal). This reflects in their 13 marketed biosimilars and 32 in the industry-leading pipeline (including the partnered ones).

Now just being good at science/manufacturing is not enough. A successful commercialisation requires physician trust, hospital contracting, and distribution reach. Sandoz emerges as a winner here also, backed by its rich history, broad portfolio and a well-spread generics business. This capability attracts partnerships as well. A case in point is the recent Sandoz-Samsung Bioepis deal for up to five biosimilars. Moreover, as competition and pricing pressure increase, the smaller players tend to cave in (e.g. Epirus Biopharmaceuticals’ collapse in 2016), and the scale leaders tend to dominate this market. This is perhaps why the biosimilar industry is moving towards an oligopoly of 8-10 major players.

Lastly, despite the relatively unattractive growth rate and profitability, generics remain an important source of resilience for Sandoz, because of the wide portfolio (1300 drugs; that partly compensates for pricing pressure), pipeline (400 candidates), and the might of their scale and commercial infrastructure. Not to forget their role in funding biosimilar expansion. In addition, we would look forward to the impetus from generic versions of coveted latest-generation weight-loss drugs in the coming years.

That said, the increasing competition from Korean players like Celltrion and Samsung Bioepis, among others, cannot be overlooked. For instance, Celltrion, which is an industry leader in developing subcutaneous formulations, has 11 biosimilars marketed currently, and an ambitious goal of taking that number to 41 by 2038. These players tend to have faster development timelines, and are increasing their global commercialisation scale. Plus, pricing pressure in this industry is real, especially after 2-3 years of a biosimilar launch.

Walking the talk

While the operational delivery was questionable during Sandoz’s last few years under Novartis, it has been nothing short of impressive since its demerger in 2023. The top line has grown at an average 8% (CGR, comparable growth rate) in 2024 and 2025, and is anticipated to grow by mid-to-high single digits in 2026. The EBITDA margin has expanded to 21.7% in 2025 from 18% in 2023, underpinned by an increasing share of high-margin biosimilars in the sales mix (30% in 2025 vs. 23% in 2023). The biosimilar sales grew at an average rate of 24% (CGR) in 2024 and 2025. Also, considering that biosimilars usually sell at 30-35% discount to the originator drugs vs. 70-80% for generics, they are more profitable products. In summary, the Swiss giant is well on track to meet its target of mid-single digit sales growth and an EBITDA margin of 24-26% by 2028.

This kind of execution is backed by dominant market share of its biosimilars – Hyrimoz (originator AbbVie’s Humira; $22bn peak sales in 2021), Pyzchiva (originator J&J’s key immunology medicine Stelara, $10.9bn sales in 2023) and Omnitrope (world’s first-ever biosimilar; for growth-hormone-related disorders) have 21%, 24% and 35% global shares, respectively. The multiple sclerosis medicine Tyruko (originator Biogen’s Tysabri; peak sales of c.$2bn) held c.17% European share as of Q4 25.

In a nutshell, full marks to the management in terms of execution.

Quality warrants a place in the portfolio

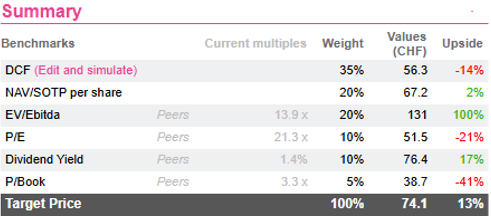

On top of the above-discussed aspects, a strong balance sheet (2026e net debt-to-EBITDA of 1.5x) and a healthy free cash flow generation backs dividends and accelerated expansion plans. A 2026e P/E of c.23x may appear expensive vis-à-vis the likes of Hikma (c.11x; BUY; UK), however, we see it as largely justified. While we may not have a massive upside on this name (restricted by fundamental valuation metrics), we still recommend Sandoz in one’s portfolio mix. After all, it is not easy to find a leader with a strong moat in an expanding market.

Subscribe to our blog

Sanofi looks cheap — but years of R&D setbacks, revolving-door CEOs, and heavy reliance on ...

Markets are cooling on a year of AI-driven speculation as debt funding tightens. AlphaValue expects ...