Casino: Debt pressure is surmounting

[dropcap]C[/dropcap]asino’s share price collapsed c.10% on Friday evening after the US short seller Muddy Waters said on Twitter that one of Casino’s subsidiaries (the finance unit of the retailer) had not filed its 2017 accounts.

This news raised fresh concerns about the company’s financial health, which has already been struggling with pressing issues such as high leverage, increasing competition in France and weakening LatAm currencies (although the operations remain healthy).

The company’s spokesperson, however, said the delay was attributable to technical reasons and this subsidiary’s accounts were already integrated into Casino 2017 consolidated results.

He also added that the concerned accounts will be filed on Saturday (31 August 2018) and shall be available on Infogreffe next week.

New details released by management

Casino (CGP) has also released some details (regarding its credit rating, French cash and working capital position) in a press release.

1. S&P has downgraded Casino’s financial rating by one notch to BB, negative perspective. However, management remains confident about its ability to deleverage the French business on the back of the €1.5bn asset disposal plan (announced in June 2018) and good sales momentum in France (and LatAm) since the beginning of the year, and particularly in July and August.

2. The Casino board, which met on 31 August 2018, believes that the Casino stock price is subject to speculative repeated attacks.

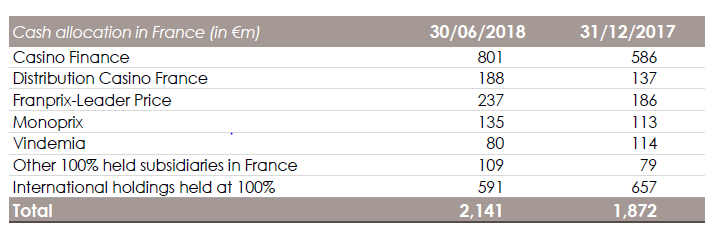

3. The French entity (includes CGP, French businesses and wholly-owned holding companies) held cash & cash equivalents worth €2.1bn at 30 June 2018 and €1.9bn at 31 December 2017. And this cash is fully available to CGP, regardless of the subsidiaries holding the cash.

4. The subsidiary under question, Casino Finance, is a fully-owned subsidiary of CGP and a cash-pooling entity for the French businesses.

The following table includes the cash of Casino Finance, the balance of cash held by of the French businesses (held 100%) that has not yet been centralised at the closing date, and the cash of international holding companies.

Source: Casino filings

Source: Casino filings

Subscribe to our blog

Alphavalue Morning Market Tip

FY results in line - Dividend cut and new restructuring plan.

AI valuations are defying reality. As three mega-IPOs worth $3.5 trillion approach, markets are ignori...

AI capex is a bubble - tokens sold below cost, no returns in sight, and $1tn invested in 2026 alone wi...