Peak Banks?

The French political instability has triggered a wave of profit taking on European Banks.

Here is the score for the 3 days of trading to the 27-08 close.

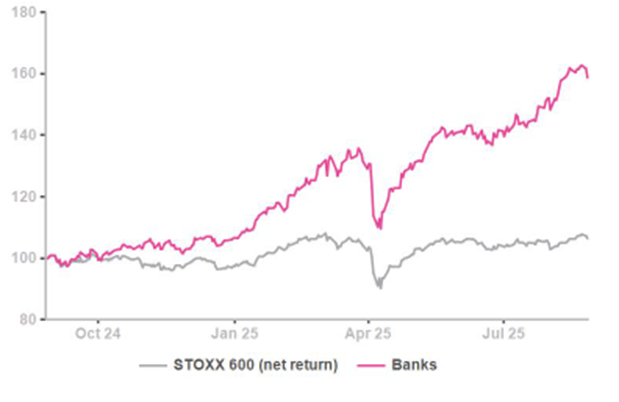

European Banks (pink) hammered since 25-08

While the trigger came from an unexpected French political corner, it is effective in forcing more cautious expectations on a sector which has been the driving force behind the strength of the Stoxx600. Italian initiatives to raise more taxes from their banks should add to worries.

Question marks about Banks, are question marks about the Stoxx600 to the extent that Banks now account for c. 12% of the index market cap and have represented c.45% of the index gain ytd.

Banks drove the Stoxx600

This strength in Banks share prices has led the sector P/Book to new highs at 1.17x, a figure last seen in 2008. One would argue that such P/Books are actually lagging the sudden surge in sector ROE from 2021. The sector ROE in 2025 is 11.2%.

High P/Book (blue) are actually lagging a surging profitability (ROEs in pink)

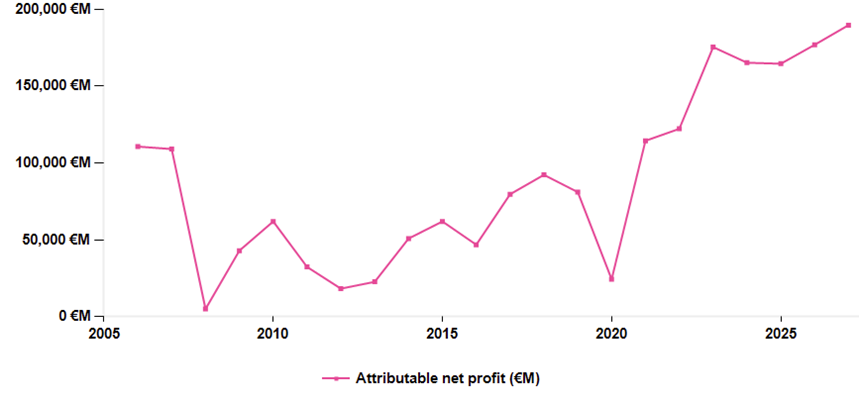

The sector presents no earnings concern with the proverbial recession and loan loss pick-up being pushed back quarter after quarter. The long earnings view is the following chart, which suggests that dividends and buy backs, essential to European investors, will continue unabated.

Banks enjoyed the rate hikes … and beyond

Even over the recent period of 2025 general earnings trimming, banking stocks have been resilient as they have actually been upgraded.

Banks’ near term earnings Upgrades

A conundrum developing

Banks on fundamentals are must-haves because they are excellent payers. The only issue is whether the state of public finances across Europe does not create again the now palpable seeds of a doom loop, for the industry: sovereign worries here (France, UK) challenging perceived balance sheet risks, higher ‘exceptional’ taxes here and there (Italy, Central Europe) and the distinct possibility that the ongoing industry consolidation (Unicredit/CBK, Mediobanca/MPS, Sabadell/BBVA) has helped push valuations a tad too high.

In a word, a degree of profit taking may be wise.

Here is the score for the 3 days of trading to the 27-08 close.

European Banks (pink) hammered since 25-08

While the trigger came from an unexpected French political corner, it is effective in forcing more cautious expectations on a sector which has been the driving force behind the strength of the Stoxx600. Italian initiatives to raise more taxes from their banks should add to worries.

Question marks about Banks, are question marks about the Stoxx600 to the extent that Banks now account for c. 12% of the index market cap and have represented c.45% of the index gain ytd.

Banks drove the Stoxx600

This strength in Banks share prices has led the sector P/Book to new highs at 1.17x, a figure last seen in 2008. One would argue that such P/Books are actually lagging the sudden surge in sector ROE from 2021. The sector ROE in 2025 is 11.2%.

High P/Book (blue) are actually lagging a surging profitability (ROEs in pink)

The sector presents no earnings concern with the proverbial recession and loan loss pick-up being pushed back quarter after quarter. The long earnings view is the following chart, which suggests that dividends and buy backs, essential to European investors, will continue unabated.

Banks enjoyed the rate hikes … and beyond

Even over the recent period of 2025 general earnings trimming, banking stocks have been resilient as they have actually been upgraded.

Banks’ near term earnings Upgrades

A conundrum developing

Banks on fundamentals are must-haves because they are excellent payers. The only issue is whether the state of public finances across Europe does not create again the now palpable seeds of a doom loop, for the industry: sovereign worries here (France, UK) challenging perceived balance sheet risks, higher ‘exceptional’ taxes here and there (Italy, Central Europe) and the distinct possibility that the ongoing industry consolidation (Unicredit/CBK, Mediobanca/MPS, Sabadell/BBVA) has helped push valuations a tad too high.

In a word, a degree of profit taking may be wise.

Subscribe to our blog

A $330 share price, 40x earnings expected five years from now, and growth funded by SoftBank: wh...

European defence is no longer the cozy oligopoly it once was. Rising competition from AI-driven sta...