Who are the Losers of the Oil and Gas Boom?

The current boom cycle in oil and gas has unbelievably benefited the companies in AlphaValue’s Oils equity research coverage. Integrated Oils have particularly been the clear winners (+42% YTD) ― stronger than the previous boom cycles such as 2008 and 2011-14 thanks to more-than-ever robust balance sheets.

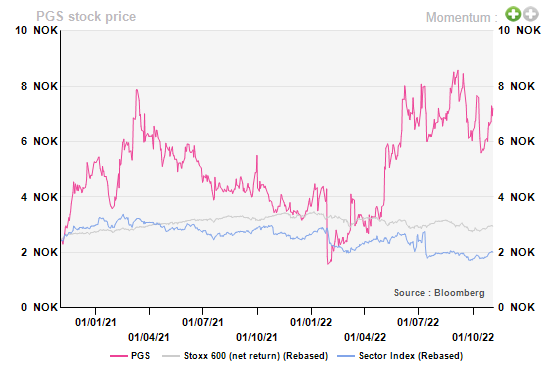

The same outstanding performance, however, is not observed in the Oil Services subsector, trading 25% down ytd. Several issues including financing troubles, project delays, and stumbling revenue recognition have stemmed the sector’s performance, albeit an overwhelmingly positive narrative. Let’s look at PGS, a Norwegian-integrated company in marine geophysics. PGS sells multiclient data, contract acquisition, and imaging solutions and benefits from flexibility as it has done so far in 2022.

PGS has gained 79% ytd and the market seems to have been appreciating the momentum. The stock, however, is still trading significantly below 2008 and 2012 levels, a performance that is in stark contrast to the Oils sector and the Integrated Oils subsector performance.

The stock, we believe, is a strong call option for daring investors as underlying financing issues remain sticky. Cash flow from operations rose to the highest level since 2018 but a very significant portion of revenue growth was driven by higher prices (35% in contract rates). Higher prices are great, but higher volumes are even better as they signal a more sustainable outlook.

AlphaValue provides unbiased, reliable and independent equity research. We believe that this is key to ensuring market integrity. Find out more about us here.